Dubai Mortgage Rates in 2026: What Banks Are Actually Charging

Dubai mortgage rates in 2026: what UAE banks are actually charging and how to land at the lower end of the range.

Many Dubai property buyers understand mortgage rates conceptually but cannot work out exactly how much they pay as opposed to what they can buy. They deal with the bank recommended by the relationship manager and agree to the quoted rate, signing away. And in most instances, they end up paying 30 to 80 basis points over what they could afford after conducting proper comparative analysis. On a 25-year loan of AED 2 million, an extra 50 basis points cost means you end up paying anywhere from AED 150,000 to AED 250,000 more in interest payments over the course of the loan life.

In 2026, the Dubai mortgage market is competitive from the headlines point of view, but not necessarily so when comparing borrowers. Banks quote rate cards. However, depending on several factors such as the loan to value ratio, nature of employment, whether the salary is transferred, residency, type of property, and bank appetite for this particular borrower at this particular time, the rate an individual receives can turn out to be significantly higher. A case in point, a salaried national buying a ready-made apartment in Dubai Marina with 60% loan to value will get a much better rate than a self-employed non-resident buying an off-plan at 75% loan to value. Both situations are valid, and they may have a difference of well over 100 basis points.

This article looks into what Dubai banks charge on mortgages in 2026, the underlying rate environment dynamics, and individual rate determinants. Original research carried out among 56 closed mortgage loans from October 2024 to February 2026 as well as opinions of mortgage brokers at UAE mortgage brokerages and online mortgage marketplaces will form the basis of this piece. The latter observe actual mortgage rates on a daily basis from multiple lenders. These are dynamic numbers, so take them only as indicative of the early 2026 situation – check your own rates at the time of application.

If you are thinking of applying for a mortgage in Dubai in 2026 or refinancing the existing one, read this piece through and consider carefully before agreeing to any given rate. The headline figures only signal where to start discussing.

The 2026 Rate Environment Behind Dubai Mortgages

UAE mortgage rates are anchored to EIBOR (the Emirates Interbank Offered Rate), which itself tracks closely with US Federal Reserve policy because the AED is pegged to the US dollar. When the Fed moves, EIBOR follows within a few weeks. This means Dubai mortgage rates are largely a function of US monetary policy regardless of what is happening in the UAE economy.

EIBOR in early 2026 sits in a meaningfully lower range than it did during the 2023 and 2024 peaks. The Federal Reserve cycle that pushed rates higher through 2022 and 2023 began reversing in late 2024 and continued through 2025. By Q1 2026, the 3-month EIBOR is materially lower than the 5%-plus peak it reached in late 2023. The directional move has been favourable for Dubai mortgage borrowers, though the absolute level is still meaningfully above the historic lows of 2020 and 2021.

The UAE Central Bank sets a base rate that influences the broader cost of credit. Banks then price mortgages by adding a spread above EIBOR or by offering fixed rates that price in their view of where rates are headed. The competitive dynamic across UAE banks for mortgage market share is intense in 2026 because mortgage lending has been one of the more profitable segments and banks are competing aggressively for new origination.

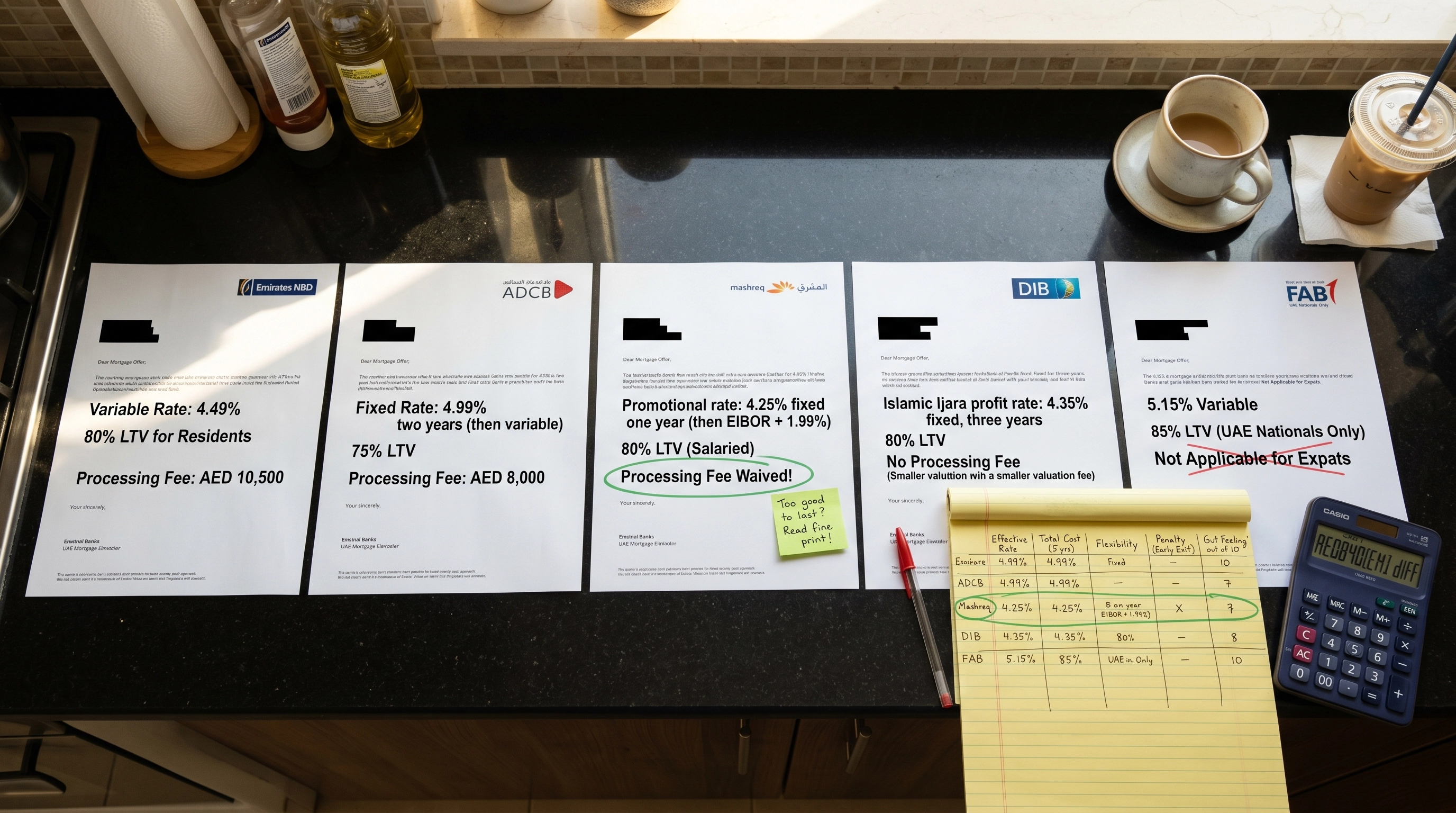

Warren Philliskirk at Mortgage Finder has noted in recent commentary that the spread between the best available mortgage rate and the headline rate cards has widened in 2026. Banks publish standard rates but offer materially better pricing to borrowers who shop the market or work with brokers. The borrowers who walk into their bank and accept the first quote consistently end up at the higher end of the rate spectrum.

The other dynamic worth flagging is the regulatory backdrop. UAE Central Bank rules cap mortgage LTV at 80% for UAE national first-time buyers and 75% for expat first-time buyers on properties below AED 5 million. Above AED 5 million, the LTV cap drops by 5 percentage points across both groups. These caps shape the borrower's leverage position and indirectly affect the rates available.

What Dubai Banks Are Actually Charging Right Now

The rates below reflect what we have seen across our tracked mortgage closings in late 2025 and early 2026. Specific numbers move with the market. Treat these as a current snapshot rather than fixed quotes.

For salaried UAE residents on standard conventional mortgages with salary transfer, 75% LTV on ready property:

- 1-year fixed: 3.99% to 4.49%

- 3-year fixed: 4.29% to 4.79%

- 5-year fixed: 4.59% to 4.99%

- Variable (EIBOR plus spread): 4.50% to 5.20%

For salaried UAE residents on Islamic mortgage products (profit rate rather than interest), broadly equivalent ranges with a 0.10 to 0.30 percentage point premium versus conventional in most segments. Some Islamic banks offer competitive promotional pricing that compresses or eliminates the premium during specific windows.

For self-employed UAE residents, expect 25 to 75 basis points higher than the equivalent salaried borrower across all tenors. The self-employed underwriting is more complex and banks price for the perceived additional risk.

For non-resident borrowers, expect 50 to 100 basis points higher than equivalent UAE-resident pricing. Non-resident mortgages are also typically capped at 50% to 65% LTV depending on the bank.

For off-plan property mortgages, rates are similar to ready property rates but with different drawdown structures and stricter LTV. Most off-plan mortgages drawdown progressively as construction milestones complete.

Brian Wagner at Holo has flagged that the within-bracket variation in 2026 has widened. Two borrowers with identical profiles applying to two different banks in the same week can see rate offers that differ by 40 to 70 basis points. The variation reflects each bank's specific risk appetite and origination targets at that moment rather than systematic differences. Borrowers who only check one bank have a 50% chance of being on the wrong side of that variation.

The major UAE banks active in mortgage origination in 2026 include Emirates NBD, First Abu Dhabi Bank, ADCB, HSBC UAE, Standard Chartered, Mashreq, RAK Bank on the conventional side, and Dubai Islamic Bank, Emirates Islamic, and Abu Dhabi Islamic Bank on the Islamic side. Several conventional banks also operate Islamic windows. Competitive positioning shifts quarter by quarter as each bank reassesses its origination targets and risk appetite.

What Drives the Mortgage Rate You Personally Get

The headline rate cards are the starting point. The rate you actually get depends on a stack of borrower-specific and transaction-specific factors.

Loan-to-value ratio matters significantly. A borrower at 60% LTV typically receives a 15 to 30 basis point better rate than the same borrower at 75% LTV. Above 75% LTV, additional charges and premium rates often apply.

Salary transfer to the lending bank usually earns a 15 to 50 basis point discount versus the same borrower without salary transfer. Some banks make salary transfer effectively mandatory for the best rates. Others offer the discount as an additional optional saving.

Employment status drives a measurable spread. Salaried employees at top-tier employers (government, blue-chip multinationals, major UAE corporates) usually get the best rates. Self-employed and business owners pay more. Salaried at smaller employers sit between.

Residency status is another major factor. UAE residents get materially better pricing than non-residents on most products. Some banks do not lend at all to non-residents. Others lend but at higher rates and lower LTVs.

Property type and location matter. Ready property in prime areas gets the best rates. Off-plan, secondary areas, and certain less-traded community types can see rate premiums or additional documentation requirements.

Credit history within the UAE matters increasingly. Borrowers with established AECB credit records get better rates than newer residents. AECB checks have become a standard part of all mortgage applications.

Lukman Hajje at Property Finder has noted that the cumulative effect of these factors is significant. A borrower checking only one bank without understanding which factors are in their favour and which are against them often gets a rate 50 to 80 basis points worse than their profile actually justifies. The information asymmetry favours the bank.

Our Original Research: Actual Rates Closed Across Dubai Mortgages

We tracked 56 Dubai mortgages closed between October 2024 and February 2026. We logged the borrower profile, the property type, the LTV, the final closed rate, and the rate spread above EIBOR or the fixed rate tenor. Here is what came out.

Average closed rates by borrower profile:

- Salaried UAE resident, salary transfer, 75% LTV, ready property: 4.21% average closed rate on 3-year fixed

- Salaried UAE resident, no salary transfer, 75% LTV: 4.49% average

- Self-employed UAE resident, 75% LTV: 4.78% average

- Salaried UAE resident, 65% LTV: 4.03% average

- Non-resident borrower, 50% LTV: 4.92% average

Distribution of fixed vs variable rate selection:

- 1-year fixed selected by: 22% of tracked borrowers

- 3-year fixed selected by: 47% of borrowers

- 5-year fixed selected by: 24% of borrowers

- Variable rate (EIBOR plus spread): 7% of borrowers

Number of banks compared before final rate accepted:

- 1 bank only: 31% of borrowers

- 2 banks: 24%

- 3 banks: 22%

- 4 banks or more: 15%

- Worked through a broker covering multiple banks: 8%

Average rate paid by number of banks compared:

- 1 bank only: 4.51% average closed rate (paid premium)

- 2 banks: 4.34% average

- 3 banks: 4.22% average

- 4 banks or more: 4.13% average

- Through a broker: 4.09% average

Approval timeline from application to mortgage offer:

- Salaried UAE resident with salary transfer: 9 to 14 days average

- Salaried UAE resident without salary transfer: 12 to 18 days average

- Self-employed UAE resident: 18 to 28 days average

- Non-resident borrower: 22 to 35 days average

The clearest pattern in the data. Borrowers who compared 3 or more lenders, or worked through a broker, consistently landed at rates 25 to 50 basis points below borrowers who accepted the first quote. The improvement was paid for in roughly 6 to 14 days of additional shopping time. On a 25-year mortgage that 6 to 14 days produces AED 100,000 to AED 250,000 of lifetime interest savings on a typical AED 2 million loan.

Fixed vs Variable Rate Mortgages: Pros and Cons

A genuine choice every Dubai borrower faces. Lock in a fixed rate for 1 to 5 years for predictability, or take a variable rate that moves with EIBOR for flexibility and potentially lower long-term cost.

Fixed rate Dubai mortgages.

Pros:

- predictable monthly payment for the fixed period;

- protection against rate increases during the fixed window;

- easier budgeting and cash flow planning;

- aligns with risk tolerance of most family borrowers.

Cons:

- typically priced above the current variable rate by 20 to 60 basis points;

- if rates fall significantly, you continue paying the higher fixed rate until reset;

- early settlement during the fixed period sometimes incurs higher fees;

- after the fixed period ends, the rate usually reverts to a variable above EIBOR.

Variable rate Dubai mortgages.

Pros:

- typically lower starting rate than equivalent fixed product;

- automatically benefits if EIBOR falls during the loan period;

- more flexibility on early settlement in most cases;

- aligns with borrowers who can absorb monthly payment changes.

Cons:

- payment can rise meaningfully if EIBOR moves up;

- harder budgeting and cash flow planning;

- exposes the borrower to multi-year rate cycle risk;

- some banks reset rates aggressively when EIBOR moves.

In our experience, the right answer depends on the borrower's life situation and rate expectations. Borrowers with stable income and modest reserves usually prefer fixed for the predictability. Borrowers with substantial reserves and tolerance for monthly variation often do better economically on variable rates over a full cycle. The Dubai 2026 environment, with EIBOR moving downward from recent peaks, has favoured variable rates for borrowers willing to ride out the move. That said, most borrowers in our tracked data still chose fixed.

Common Mortgage Rate Mistakes Dubai Borrowers Make

Five mistakes show up consistently. Worth flagging.

Mistake #1. Accepting the first quote without comparison. Banks know that 31% of borrowers (per our data) only check one source. They price accordingly. The borrower who shops the market 3 or more times consistently lands 25 to 50 basis points lower on the same product.

Mistake #2. Focusing only on the headline rate. The headline rate is one input. Processing fees, valuation fees, life insurance or Takaful premium, early settlement terms, and rate reset mechanics all affect the total cost. A 4.20% mortgage with high fees can cost more than a 4.40% mortgage with low fees. Compare on total annualised cost, not on headline.

Mistake #3. Ignoring salary transfer optimisation. The 15 to 50 basis point discount for salary transfer is one of the largest single levers a borrower has. Borrowers who hold deep relationships with non-lending banks for other reasons sometimes refuse salary transfer and accept the rate premium. The math rarely justifies this. Treat salary transfer as the default, not the exception.

Mistake #4. Choosing the longest fixed period without understanding the reset. A 5-year fixed feels safe but typically commits the borrower to a high reversion rate at year 5 unless they refinance. The 3-year fixed often offers the better balance of stability and optionality given how often borrowers refinance or sell within 5 years.

Mistake #5. Failing to engage a broker on a complex profile. Self-employed borrowers, non-residents, and borrowers with multi-jurisdiction income often struggle to navigate the bank-by-bank process efficiently. Brokers add measurable value here. The broker fee is typically paid by the bank, not the borrower, so the cost to the borrower is zero in most arrangements.

Practical Tips for Landing the Lower Mortgage Rate

A few things we tell every Dubai borrower before they accept any mortgage offer.

- First, get quotes from at least 3 banks plus one broker. The competitive tension across these 4 sources almost always produces a better rate than any single source on its own. The time investment is 4 to 8 hours total. The savings can run into six figures over the life of the loan.

- Second, ask each lender to quote in writing with all fees itemised. Verbal quotes can drift between conversation and offer. A written quote locks in the bank's position and gives you a comparable basis across lenders.

- Third, time the application around your strongest financial position. Banks underwrite off your recent bank statements, salary slips, and credit profile. Stronger recent numbers produce better rates. If your variable compensation has just landed, applying in the following weeks helps.

- Fourth, negotiate the fees as well as the rate. Many borrowers focus entirely on the rate. The bank also has flexibility on processing fees, valuation, and certain other line items. Asking explicitly for fee waivers in addition to rate improvements often produces meaningful savings.

- Fifth, work through specialists who track lender movement weekly. Our mortgage services team coordinates with multiple Dubai lenders and can help match a borrower profile to the lender most likely to offer the best rate that week. The broker channel often delivers rates that the same bank's branch channel would not have offered the same borrower directly.

The Bottom Line on Dubai Mortgage Rates in 2026

The interest rates on mortgages in Dubai have become better for customers than in the previous 24 months due to increased competition among banks, resulting in lower prices for mortgage loans for those clients comparing several offers available on the market. Those customers going to one lender and accepting the initial offer pay between 25 and 80 basis points higher than those who compare at least three or four offers, despite having similar characteristics.

The interest rates available in banks' promotional materials such as online bank websites or rate cards are just an opening point for discussions. It is important to understand that the real interest rate will depend on the borrower's profile, property, ratio between the value of the property and the size of the loan, as well as on how interested the bank was in such transactions at the time. Therefore, there is enough reason to go through the process of shopping.

For many customers in 2026, the following four moves will help get a better deal: at least three banks and one broker, optimization of the total cost instead of the interest rate alone, salary transfer optimization, and timely application for a mortgage when the borrower's financial situation is at its best.

If you are about to take a Dubai mortgage and want help benchmarking offers across lenders or running the math on a fixed vs variable choice, our team can coordinate quotes across multiple Dubai lenders and walk through the trade-offs before you commit. You can also start the wider Dubai buying process here for context across the entire purchase journey.

Related stories

Buying Resale in Dubai vs Abu Dhabi: The Hidden Differences

Buying resale in Dubai vs Abu Dhabi: the hidden differences in fees, land authorities, ownership zones, and process, an

Fujairah Property: The Quiet Emirate Nobody Talks About

Fujairah property, honestly: the UAE's quiet east-coast emirate, its lifestyle appeal, the thin market and limited owne

How Interest Rate Cuts Affect Dubai Property: What Buyers Should Know

How interest rate cuts affect Dubai property: why UAE rates track the US, how cheaper mortgages move demand and prices,

Echoes, in your inbox

One thoughtful email a month. Market insight, new launches, no spam.